The Robot Market Is Quietly Decoupling From Detroit

For decades, the health of the North American industrial robotics market could be read off a single dashboard: how many robots were being ordered by automotive manufacturers. When Ford, GM, and Stellantis were retooling, the robotics industry boomed. When they paused, the industry slumped. The auto sector wasn't just the largest buyer of industrial robots — it was the buyer that mattered.

That story is ending. And the first quarter of 2026 is one of the clearest data points yet.

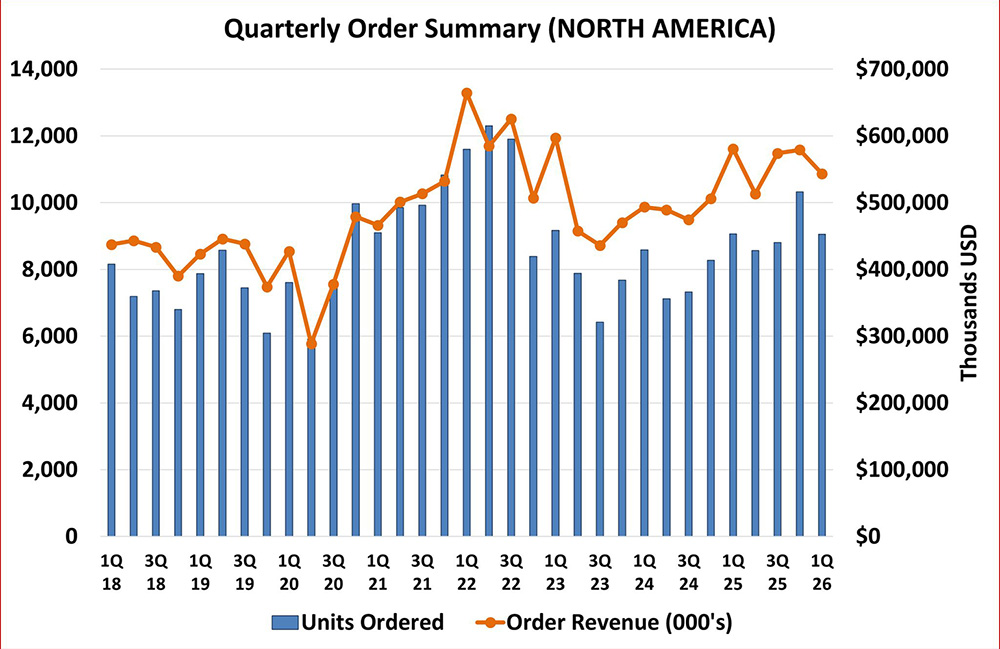

North American companies ordered 9,055 robots valued at $543 million in Q1 2026, according to new figures released by the Association for Advancing Automation (A3). On the surface, the numbers look flat: a 0.1% decline in units and a 6.4% decline in revenue compared to the same quarter last year. A casual reader might glance at those numbers and conclude the robotics market is stalled.

The casual reader would be wrong. What's actually happening underneath the headline numbers is one of the most consequential structural shifts the industry has seen in decades.

Quarterly North American robot orders from 2018-2016. Source: A3

The automotive contraction

The flat headline is being held down almost entirely by one segment. Automotive OEM orders — the major car manufacturers themselves — fell 35.1% in units and 48.2% in revenue compared to Q1 2025. That's not a wobble. That's a contraction large enough to drag the entire North American market into negative territory.

A3 attributes the drop to the cyclical nature of automotive programs. Major automakers buy robots in waves tied to product launches, plant retoolings, and electric vehicle transitions, and the timing of those waves can swing quarterly numbers dramatically. Given the size of automotive purchases relative to the total market, even a modest pause from Detroit, Tennessee, and the Mexican auto belt is enough to move the national needle.

But the automotive component suppliers — the Tier 1 and Tier 2 firms that feed the OEMs — tell a different story. Their orders are up 28.1% in units and 15.5% in revenue year over year. That divergence is typical: component suppliers run on a lag behind the OEMs they sell to, and right now they're catching up to retoolings the OEMs ordered in previous quarters. The supplier strength suggests the OEM decline is a timing issue rather than a demand collapse.

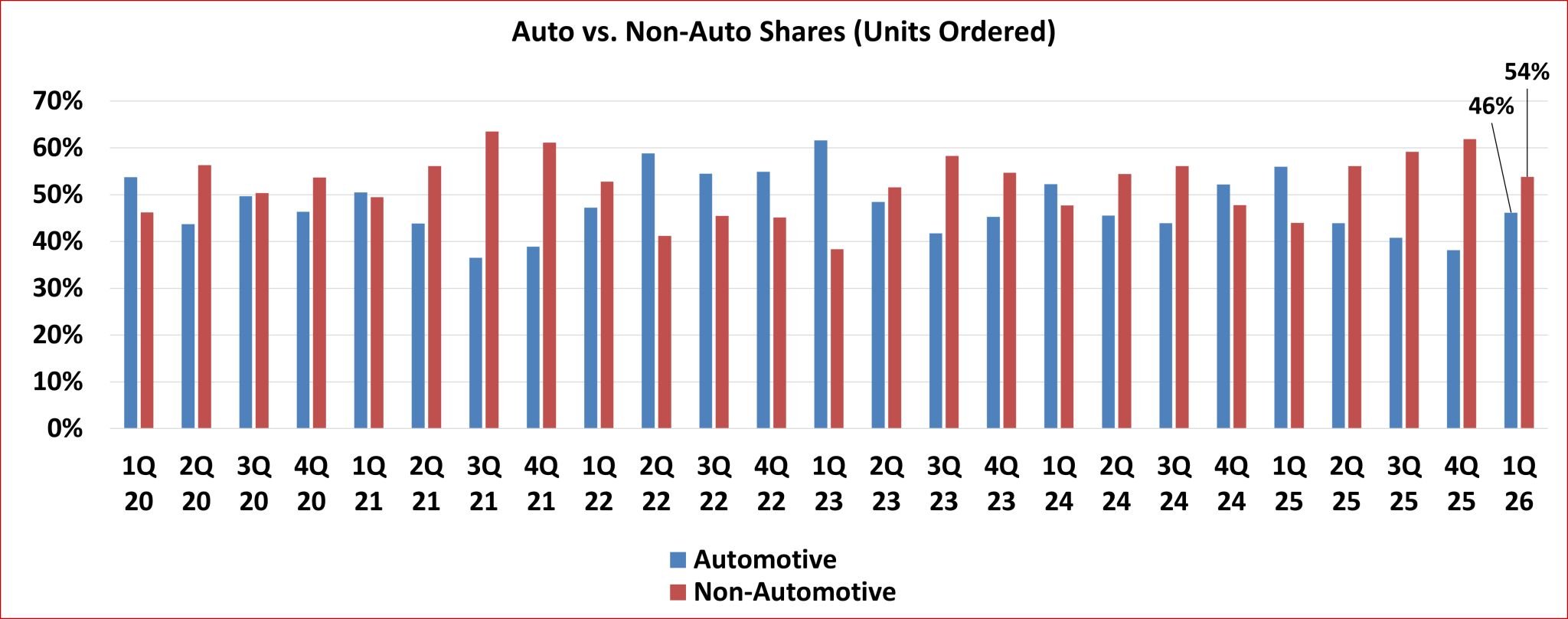

Still, the automotive industry's share of the North American robotics market is structurally shrinking. And the reason is that everyone else is buying more robots, faster.

The broadening base

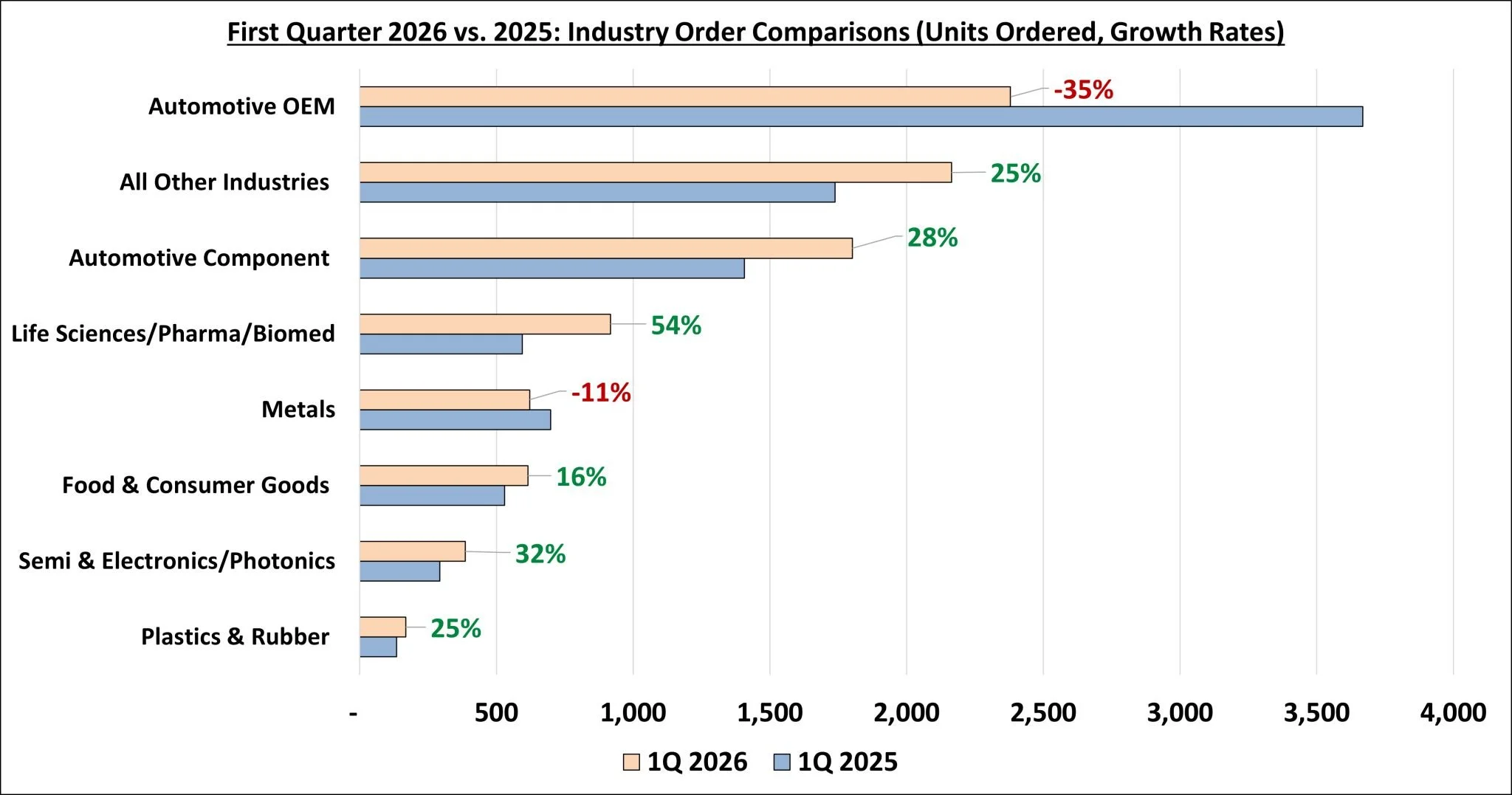

Strip out the automotive OEM contraction, and the Q1 2026 numbers tell a very different story. Almost every other industry tracked by A3 posted significant year-over-year gains in robot orders.

Life sciences, pharmaceuticals, and biomedicine led the field with a 54.1% increase in units ordered and a 70.2% increase in revenue. That's not a marginal trend. That's a sector that has fundamentally changed its mind about automation in a single year. Pharmaceutical manufacturers, contract research organizations, medical device makers, and biotech firms are buying robots at a pace that would have seemed implausible to industry observers two years ago.

Semiconductors and electronics/photonics posted a 31.7% unit gain and a 79.2% revenue gain — the disproportion between units and revenue suggests the segment is buying more expensive, more sophisticated systems, likely tied to the wave of new fab construction underway in Arizona, Texas, Ohio, and New York under the CHIPS Act.

Plastics and rubber grew 25.2% in units and 32.6% in revenue. Food and consumer goods grew 16.0% in units and 16.3% in revenue. A catch-all "all other industries" category — which includes warehousing, logistics, construction, agriculture, and a long tail of smaller verticals — grew 24.5% in units and 29.2% in revenue.

The pattern is consistent across nearly every non-automotive segment: more orders, larger orders, higher revenue per unit. The robotics market isn't shrinking. It's diversifying. And the diversification is being driven by industries that, until very recently, were not significant robot buyers.

Comparing robot orders in 2025 to 2026 so far. Source: A3

What's driving the broadening

A3 attributes the cross-industry expansion to a familiar set of pressures: labor shortages, supply chain pressures, quality requirements, and global competition. Each of those forces is doing its own work.

Labor shortages remain the most-cited reason for automation investment in industry surveys. The post-pandemic labor market hasn't loosened the way many manufacturers expected. Wages have remained elevated, turnover is persistent, and certain categories of skilled industrial labor — welders, machinists, quality inspectors — are difficult to hire at any price. Robots don't quit, don't get sick, and don't ask for raises. The math has shifted.

Supply chain pressures have pushed manufacturers toward greater operational resilience. A factory that can run a third shift unattended, or that can switch product lines without retraining a human workforce, is a factory that can absorb shocks. The Russian invasion of Ukraine, the Red Sea shipping disruptions, and the ongoing China-Taiwan tensions have all reinforced the value of operational flexibility — and robots, particularly modern programmable ones, deliver flexibility that human workforces cannot.

Quality requirements are tightening in regulated industries, particularly life sciences and semiconductors. A robot performing a repetitive task in a cleanroom environment will produce more consistent output than a human, and the consistency itself has regulatory value. For pharmaceutical manufacturers facing FDA scrutiny, or chipmakers operating at sub-nanometer tolerances, that consistency justifies the capital expense.

Global competition is the structural backdrop. North American manufacturers know that Chinese competitors are deploying robots at roughly twice the rate of US firms. Long-term competitiveness in any tradable goods category requires automation density that approaches the global frontier. Companies that wait risk being unable to compete on cost when the next downturn arrives.

Robot sales in the automotive industry compared to general industries. Source: A3

The collaborative robot story

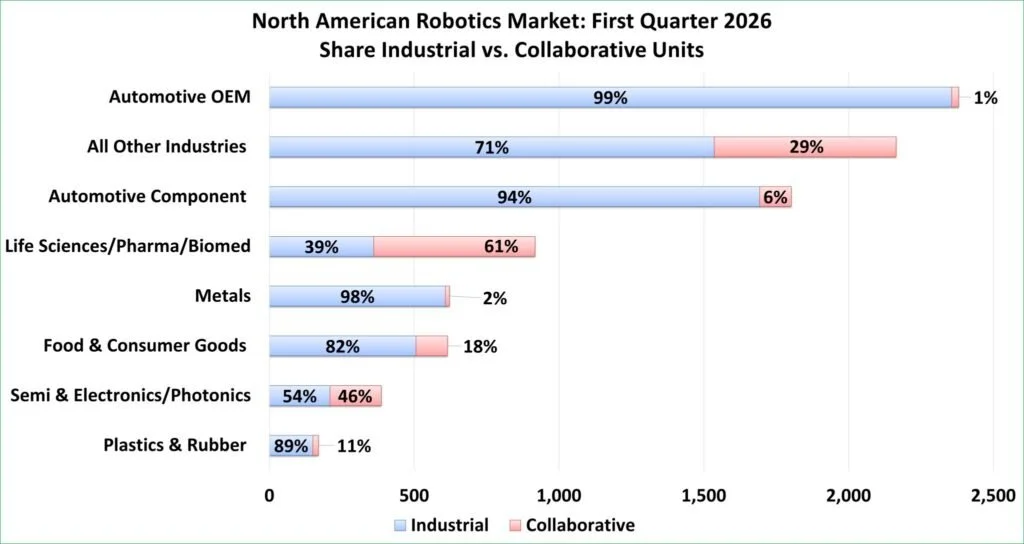

The other major story in the Q1 numbers is the rise of collaborative robots, or cobots — robots designed to work alongside human employees rather than behind safety cages.

North American companies ordered 1,637 cobots valued at $69.8 million in Q1 2026, up 55.6% in units and 78.2% in revenue year over year. Cobots now account for 18.1% of all robot units ordered and 12.9% of total order revenue.

Those numbers understate the importance of what's happening. Cobots have historically been a niche product — useful for specific applications where humans and robots needed to share workspace, but expensive on a per-task basis compared to traditional industrial robots. They were considered a small, slow-growing corner of the market.

The Q1 data suggests cobots have crossed an adoption threshold in several key industries. In life sciences, pharmaceuticals, and biomedicine, cobots accounted for 60.7% of total robot orders. In semiconductors and electronics/photonics, cobots were 45.9% of orders. In the "all other industries" category, they were 29.0%. These are not niche numbers. In two major industrial segments, more than half of all new robots being deployed are designed to work alongside humans rather than replace them.

What's changed? Several things. Cobot prices have come down significantly as Chinese and European manufacturers have entered the market. Cobot capabilities have expanded — modern cobots can lift more, work faster, and operate with finer precision than their predecessors. And cobot deployment has gotten easier, with simplified programming interfaces that let plant engineers reconfigure tasks without specialized robotics expertise.

The broader implication is that the deployment model is changing. The traditional industrial robotics image — caged cells with one robot doing one task in isolation — is giving way to mixed human-robot workflows where the robots are flexible, redeployable, and integrated into existing operations. That's a fundamentally different value proposition, and it's bringing automation into facilities that would never have considered traditional industrial robots.

North American cobot sales compared to industrial robot sales. Source: A3

The signal beneath the noise

Alex Shikany, executive vice president at A3, summarized the data carefully. "The broader takeaway from the first quarter is that automation demand is becoming more diverse in terms of industries, applications, and deployment models. That is an important signal for the long-term health of the market."

He's right, and the diversification matters more than the flat headline number suggests. A robotics market that lives or dies on Detroit's quarterly capex decisions is a fragile market. A robotics market that is simultaneously selling into pharmaceutical clean rooms, chip fabs, food processing plants, plastics extruders, and a long tail of general manufacturing is a resilient one. The Q1 numbers are the clearest sign yet that the resilient market has arrived.

For policymakers and economic development professionals, the takeaway is worth sitting with. Workforce displacement debates in the United States have historically focused on the automotive sector — what happens to the line workers in Michigan and Ohio when the next wave of robots arrives. That framing is now incomplete. The next wave of robots is arriving in pharmaceutical fill-finish operations in North Carolina, in chip fab construction in Phoenix, in food processing plants across the Midwest, in third-tier industrial suppliers in dozens of mid-sized metros.

The geography of automation is broadening alongside the industry mix. The questions that policymakers and educators have been asking about Detroit need to be asked about Memphis, Greenville, Phoenix, and dozens of other cities now. Workforce retraining programs designed for displaced auto workers may not map cleanly onto displaced pharma technicians or food processing operators. Building codes, workplace safety regulations, and liability frameworks designed around traditional industrial robotics may not fit mixed human-cobot workflows.

For investors and operators, the signal is clearer still. The robotics market is no longer a cyclical bet on Detroit. It's a structural bet on the broader industrial economy. And that economy, judging by Q1, is buying more robots than ever — just not the kind of robots, in the kind of factories, that the industry's old playbooks were written for.

The headline number was flat. Everything underneath it is moving.